Financial Reporting Valuations

PP&E Valuations provide professional property, plant and equipment valuation services for financial reporting purposes.

The benefits of obtaining an independent valuation include:

Are you 100% confident that your carrying values comply with your reporting requirements?

The benefits of obtaining an independent valuation include:

- Declaration of the correct fair values;

- Compliance with accounting standards;

- Compliance with Directors' responsibilities; and

- Satisfy auditors and avoid qualified opinions.

Are you 100% confident that your carrying values comply with your reporting requirements?

Valuations for financial reporting compliance

Valuations are often required for compliance with the following Australian accounting standards or international equivalents;

Fair Value and Market Value

Fair Value is the key basis of value required for financial reporting purposes. It is defined in AASB116 Property, Plant and Equipment as "the amount for which an asset could be exchanged or a liability settled between knowledgeable willing parties in an arm’s length transaction".

In preparing a valuation for financial reporting purposes, the basis of value adopted is market value with specific underlying assumptions based upon whether the asset is specialised or non-specialised and operational or non-operational.

The International Valuation Standards defines market value as "the estimated amount for which a property should exchange on the date of valuation between a willing buyer and willing seller in an arm’s-length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently, and without compulsion".

In preparing a valuation for financial reporting purposes, the basis of value adopted is market value with specific underlying assumptions based upon whether the asset is specialised or non-specialised and operational or non-operational.

The International Valuation Standards defines market value as "the estimated amount for which a property should exchange on the date of valuation between a willing buyer and willing seller in an arm’s-length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently, and without compulsion".

Approaches to Determining Market Value

There are three approaches to determining market value namely;

The market comparison approach seeks to determine the current value of an asset by reference to recent comparable transactions involving the sale of similar assets.

The market comparison approach is generally appropriate for assets for which an established market exists such as real estate, motor vehicles, general plant and equipment, etc.

The income approach seeks to determine the current (present) value of anticipated future economic benefits associated with the assets. The net cash flows are projected over the appropriate period and discounted back to a net present value using an appropriate discount rate that reflects cost of capital, risk and required return.

The income approach values, by default, both tangible and intangible assets. Therefore, in many instances the income approach is not considered an appropriate approach when seeking only to determine the value of the underlying tangible assets.

The depreciated replacement cost (DRC) is the estimated current cost of replacement of the asset with a similar asset which is not necessarily an exact reproduction but which has similar service potential and function (plus where applicable and amount for installation), less an amount for depreciation in the form of accrued physical wear and tear, economic and functional obsolescence.

The DRC is an acceptable surrogate method for arriving at a market-related value. The method is commonly applied in a valuation situation involving an asset where there is no readily available or otherwise dependable market data to analyse in developing a market value estimate.

Optimisation may also be utilised where we are of the opinion that the existing asset can be hypothetically replaced with a modern equivalent that provides the same functionality as the subject asset. This approach is sometimes referred to as Depreciated Optimised Replacement Cost (DORC).

The DRC based market values for the tangible assets assume the business is ongoing and profitable and the profits of the business would justify carrying the equipment at the nominated market values in the accounts of the business.

- the market comparison approach;

- the income approach; and

- the depreciated replacement cost approach.

The market comparison approach seeks to determine the current value of an asset by reference to recent comparable transactions involving the sale of similar assets.

The market comparison approach is generally appropriate for assets for which an established market exists such as real estate, motor vehicles, general plant and equipment, etc.

The income approach seeks to determine the current (present) value of anticipated future economic benefits associated with the assets. The net cash flows are projected over the appropriate period and discounted back to a net present value using an appropriate discount rate that reflects cost of capital, risk and required return.

The income approach values, by default, both tangible and intangible assets. Therefore, in many instances the income approach is not considered an appropriate approach when seeking only to determine the value of the underlying tangible assets.

The depreciated replacement cost (DRC) is the estimated current cost of replacement of the asset with a similar asset which is not necessarily an exact reproduction but which has similar service potential and function (plus where applicable and amount for installation), less an amount for depreciation in the form of accrued physical wear and tear, economic and functional obsolescence.

The DRC is an acceptable surrogate method for arriving at a market-related value. The method is commonly applied in a valuation situation involving an asset where there is no readily available or otherwise dependable market data to analyse in developing a market value estimate.

Optimisation may also be utilised where we are of the opinion that the existing asset can be hypothetically replaced with a modern equivalent that provides the same functionality as the subject asset. This approach is sometimes referred to as Depreciated Optimised Replacement Cost (DORC).

The DRC based market values for the tangible assets assume the business is ongoing and profitable and the profits of the business would justify carrying the equipment at the nominated market values in the accounts of the business.

Classification of Assets

In determining which approach is the most appropriate to adopt, it is necessary for the valuer to classify the assets as specialised or non-specialised and operational or non-operational.

Specialised or Non-Specialised Assets

Assets may be specialised or non-specialised in whole or part. We assess the degree of specialisation, having regard to the following:

Specialised operational assets, by their nature, lack market evidence on which to base a market value assessment and accordingly, these require a replacement cost valuation methodology. Consequently such assets are sub-categorised as replacement cost based assets and the market value with continuing use is derived by a depreciated replacement cost approach.

Operational or Non-Operational Assets

Operational assets are those which are utilised in the operation of the entity and are held for the continued use or service potential for the near future.

Non-operational assets are those which are not integral to the operation of the entity and are valued on a realisable value basis. That is, the amount that could be achieved if the assets were offered to the market separate to the operational assets of the entity.

Specialised or Non-Specialised Assets

Assets may be specialised or non-specialised in whole or part. We assess the degree of specialisation, having regard to the following:

- The use to which the asset is put;

- The degree of special adaptation;

- The location;

- Whether the category of asset has a readily definable market; and

- Guidance by the Directors and/or technical staff of the entity.

Specialised operational assets, by their nature, lack market evidence on which to base a market value assessment and accordingly, these require a replacement cost valuation methodology. Consequently such assets are sub-categorised as replacement cost based assets and the market value with continuing use is derived by a depreciated replacement cost approach.

Operational or Non-Operational Assets

Operational assets are those which are utilised in the operation of the entity and are held for the continued use or service potential for the near future.

Non-operational assets are those which are not integral to the operation of the entity and are valued on a realisable value basis. That is, the amount that could be achieved if the assets were offered to the market separate to the operational assets of the entity.

AASB3 Business Combinations

Under AASB3 as of the acquisition date, the acquirer shall recognise, separately from goodwill, the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree. The acquirer shall measure the identifiable assets acquired at their acquisition-date fair values.

PP&E Valuations has extensive experience in undertaking valuations for Purchase Price Allocation (PPA) purposes to satisfy the requirements of AASB3.

PP&E Valuations has extensive experience in undertaking valuations for Purchase Price Allocation (PPA) purposes to satisfy the requirements of AASB3.

AASB5 Non-Current Assets Held for Sale and Discontinued Operations

AASB5 stipulates that an entity shall measure a non-current asset (or disposal group) classified as held for sale at the lower of its carrying amount and fair value less costs to sell. This recoverable amount is often different to the fair value assuming continued use and will require a write down to the asset value.

We are experienced in estimating the recoverable amount of a wide range of assets, including specialised and non-specialised assets.

We are experienced in estimating the recoverable amount of a wide range of assets, including specialised and non-specialised assets.

AASB13 Fair Value Measurement

AASB13 a) defines fair value; b) sets out in a single Standard a framework for measuring fair value; and c) requires disclosures about fair value measurements.

Our valuation reports for financial reporting purposes comply with the requirements of this Standard.

Our valuation reports for financial reporting purposes comply with the requirements of this Standard.

AASB116 Property, Plant and Equipment

The principal issues in accounting for property, plant and equipment are the recognition of the assets, the determination of their carrying amounts and the depreciation charges and impairment losses to be recognised in relation to them.

An item of property, plant and equipment that qualifies for recognition as an asset shall be measured at its cost, or in respect of not-for-profit entities, where an asset is acquired at no cost, or for a nominal cost, the cost is its fair value as at the date of acquisition.

After recognition, an entity shall choose either the cost model or the revaluation model as its accounting policy and shall apply that policy to an entire class of property, plant and equipment.

Cost Model

After recognition as an asset, an item of property, plant and equipment shall be carried at its cost less any accumulated depreciation and any accumulated impairment losses.

Revaluation Model

After recognition as an asset, an item of property, plant and equipment whose fair value can be measured reliably shall be carried at a revalued amount, being its fair value at the date of the revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses.

Revaluations shall be made with sufficient regularity to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the end of the reporting period.

Componentisation

Under AASB116 Property, Plant and Equipment an entity is required to identify and depreciate the various components of an asset separately if they have differing asset lives and are significant relative to the total cost of the item.

This relates not only to new acquisitions and capital projects but also to the revaluation of assets for financial reporting purposes. It also affects both property and plant & equipment assets.

Our plant & equipment valuation reports separately list and value all material assets and their individual component assets where appropriate. For example, a mining dump truck will typically have the engine and tyres listed and valued as separate components as they have different asset lives and therefore depreciation profiles to the body of the truck.

Many property valuations do not provide values at the appropriate level of componentisation to allow the entity to report correctly. Our property valuation reports separately list and value the individual component assets. For example:

An item of property, plant and equipment that qualifies for recognition as an asset shall be measured at its cost, or in respect of not-for-profit entities, where an asset is acquired at no cost, or for a nominal cost, the cost is its fair value as at the date of acquisition.

After recognition, an entity shall choose either the cost model or the revaluation model as its accounting policy and shall apply that policy to an entire class of property, plant and equipment.

Cost Model

After recognition as an asset, an item of property, plant and equipment shall be carried at its cost less any accumulated depreciation and any accumulated impairment losses.

Revaluation Model

After recognition as an asset, an item of property, plant and equipment whose fair value can be measured reliably shall be carried at a revalued amount, being its fair value at the date of the revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses.

Revaluations shall be made with sufficient regularity to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the end of the reporting period.

Componentisation

Under AASB116 Property, Plant and Equipment an entity is required to identify and depreciate the various components of an asset separately if they have differing asset lives and are significant relative to the total cost of the item.

This relates not only to new acquisitions and capital projects but also to the revaluation of assets for financial reporting purposes. It also affects both property and plant & equipment assets.

Our plant & equipment valuation reports separately list and value all material assets and their individual component assets where appropriate. For example, a mining dump truck will typically have the engine and tyres listed and valued as separate components as they have different asset lives and therefore depreciation profiles to the body of the truck.

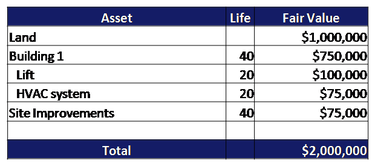

Many property valuations do not provide values at the appropriate level of componentisation to allow the entity to report correctly. Our property valuation reports separately list and value the individual component assets. For example:

Example of property valuation for financial reporting purposes showing the value of component assets.

AASB117 Leases

Leased assets are classified under AASB117 as either finance leases or operating leases. If a lease is classified as a finance lease, the fair value of the asset is required to establish the amount of the asset and liability recorded by the entity on its balance sheet.

For leases of land and buildings special rules apply. For all property, other than investment property, land and buildings have to be considered separately for classification as either a finance lease or an operating lease.

AASB140 allows Investment Property held by a lessee to be accounted for as a finance lease under AASB117, subject to further special rules. Firstly, no allocation is made between the land and buildings. Secondly, the fair value is recognised as the value subject to the lessee’s future liabilities under the lease.

The International Valuation Standards Committee considers that in each case the requirement to establish the fair value of the leased asset under AASB117 is met by the Valuer reporting the Market Value. For leases of real estate, this is the Market Value of the lease interest held by the lessee. For leases of other assets, it is normally the Market Value of the asset unencumbered by the lease, as the liability is recorded separately.

For leases of land and buildings special rules apply. For all property, other than investment property, land and buildings have to be considered separately for classification as either a finance lease or an operating lease.

AASB140 allows Investment Property held by a lessee to be accounted for as a finance lease under AASB117, subject to further special rules. Firstly, no allocation is made between the land and buildings. Secondly, the fair value is recognised as the value subject to the lessee’s future liabilities under the lease.

The International Valuation Standards Committee considers that in each case the requirement to establish the fair value of the leased asset under AASB117 is met by the Valuer reporting the Market Value. For leases of real estate, this is the Market Value of the lease interest held by the lessee. For leases of other assets, it is normally the Market Value of the asset unencumbered by the lease, as the liability is recorded separately.

AASB136 Impairment

AASB113 stipulates that an entity cannot carry assets at more than their recoverable amount. The recoverable amount of an asset or a cash-generating unit is the higher of its fair value less costs to sell and its value in use. The impairment test applies equally to an individual asset or a cash-generating unit.

If there are indicators that assets may be impaired, valuations may be needed to ensure you are not overstating the value of assets. A sudden impairment test can impact on results, timely financial reporting and unqualified auditor sign-off.

By obtaining regular revaluations and impairment reports you can proactively manage your compliance with AASB136.

This will often avoid nasty, untimely surprise write-downs.

If there are indicators that assets may be impaired, valuations may be needed to ensure you are not overstating the value of assets. A sudden impairment test can impact on results, timely financial reporting and unqualified auditor sign-off.

By obtaining regular revaluations and impairment reports you can proactively manage your compliance with AASB136.

This will often avoid nasty, untimely surprise write-downs.

AASB140 Investment Property

Investment property is property (land or a building – or part of a building – or both) held (by the owner or by the lessee under a finance lease) to earn rentals or for capital appreciation or both, rather than for:

(a) use in the production or supply of goods or services or for administrative purposes; or

(b) sale in the ordinary course of business.

Therefore, an investment property generates cash flows largely independently of the other assets held by an entity. This distinguishes investment property from owner-occupied property.

Investment property may be measured at fair value. As discussed above, fair value is assessed on the basis of market value subject to particular assumptions.

Our valuers are continually undertaking market valuations of property and plant & equipment assets and are cognisant of the nuances that sometimes need to be taken into account to comply with AASB140.

(a) use in the production or supply of goods or services or for administrative purposes; or

(b) sale in the ordinary course of business.

Therefore, an investment property generates cash flows largely independently of the other assets held by an entity. This distinguishes investment property from owner-occupied property.

Investment property may be measured at fair value. As discussed above, fair value is assessed on the basis of market value subject to particular assumptions.

Our valuers are continually undertaking market valuations of property and plant & equipment assets and are cognisant of the nuances that sometimes need to be taken into account to comply with AASB140.

AASB141 Agriculture

PP&E Valuations staff have experience in undertaking valuations for compliance with AASB141 in regards biological assets such as:

Simply contact us to arrange valuations for financial reporting purposes.

- Vines;

- Orchards; and

- Plantations.

Simply contact us to arrange valuations for financial reporting purposes.